After the Clarity Act cleared the Senate Banking Committee, SEC Chairman Paul Atkins is anticipated to roll out an ‘innovation exemption‘ framework for tokenized stock trading, opening the door to 24/7 on-chain equity markets on regulated Alternative Trading Systems.

The tokenized stock market isn’t waiting on legislators to catch up.

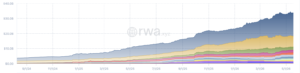

Data demonstrates distributed cost hitting $33.7 billion, up 21% in the last 30 days, with month-to-month transfer volume attaining $3.03 billion. That momentum gives the regulatory push a concrete market context, now not just policy abstraction.

Bullish signal for RWA tokenization infrastructure and compliant on-chain equity platforms.

How the SEC’s Tokenized Stock Framework and ATS Infrastructure Actually Work, and Why the DTC Pilot Is the Real Foundation

The mechanism here is well worth understanding exactly. The SEC’s proposed ‘innovation exemption’ isn’t not a wholesale rewrite of securities regulation.

A January 2026 joint staff assertion from 3 SEC divisions made the regulatory posture explicit: tokenization does not regulate the fundamental characteristics of a protection, and present disclosure obligations, custodial necessities, and investor protections persist to apply regardless of whether a stock trades on a blockchain ledger.

The practical infrastructure is supported by the DTC Pilot, a 3-year no-action granted to DTCC’s DTC in December 2025.

That pilot is restricted to highly liquid, DTC-eligible securities and needs actual-time regulatory observability and granular participant reporting – obligations with the intention to bind any ATS plugging into the same agreement rails. In March 2026, the SEC permitted Nasdaq’s rule change to permit trading of tokenized variations of DTC-eligible equities and ETPs, using the equal ticker, market policies, and economic rights as the underlying shares.

The Atkins framework expands this logic further. Bloomberg reporting suggests the plan covers both tokenized stocks issued directly by or on behalf of issuers and third-party tokenized stocks without a direct provider association, a distinction that matters notably for secondary-market liquidity and optional trading system layout.

Those two categories carry different disclosure duties and custodial structures. They are not the same thing.

Ondo, constructed on Ethereum, presently instructions 60% of the on-chain stock market. Tokenized Circle Group stocks represents around $212 million in value; tokenized NVIDIA Corp. Sits at $89.3 million; tokenized Tesla Inc. At $85.4 million.

Those 3 names alone account for more than 25% of overall tokenized stock value throughout 266,000+ holders and 83,257 monthly active wallets.

Can the Clarity Act Clear 60 Senate Votes – and What Does Each Scenario Mean for Blockchain Regulation?

The CLARITY Act’s path to law is the pivotal variable. The bill clears its next obstacle – a Senate Banking Committee vote – but the floor needs 60 votes. Republicans hold 43 seats, meaning pro-crypto advocates need at the least 17 Democratic votes to break a filibuster. Polymarket recently prices the possibility of a 2026 floor vote at 64%.

If surpassed, the CLARITY Act shifts primary regulatory oversight of crypto trading from the SEC to the CFTC – with a selected carve-out keeping digital securities oversight at the SEC.

That jurisdictional line isn’t cosmetic. It shows which rulebook governs tokenized equity ATS platforms, how margin and leverage rules apply, and which agency has enforcement authority over platforms like Ondo.

If Seventeen or more Democratic senators back the bill; the CLARITY Act passes in July 2026, the SEC’s innovation exemption framework release concurrent with latest ATS licensing, and tokenized stock disbursed value, already at $1.43 billion, expands towards $5 billion by year-end as institutional platforms gain regulatory cover.

NYSE has already tapped Securitize to expand tokenized securities markets, and at the least one additional U.S. exchange has mentioned plans for 24/7 tokenized trading with stablecoin settlement, signaling that Nasdaq’s Pilot model will not continue to be particular regardless of what Congress does.

The SEC’s broader regulatory posture under Atkins is clearly moving closer to structured engagement instead of enforcement-first friction.

The blockchain regulation framework is shifting. The 17 Democratic votes are the only variable the market can’t price with confidence yet.