The June 2026 crypto rout just removed $62 billion in integrated market capitalization from public companies protecting Bitcoin as a treasury asset.

MicroStrategy, Tesla, and Marathon Digital are causing the damage. The significant matters now isn’t whether the losses are recoverable; it is whether the whole structural model that produced them was feasible to start with.

Corporate Bitcoin holdings hastened after MicroStrategy’s initial $250 million allocation in August 2020, structured explicitly as a hedge against dollar debasement.

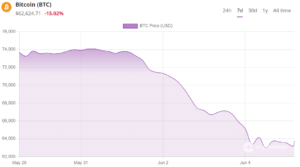

By overdue 2025, more than 200 public corporations together held an assessed $150 billion in digital assets. They bought near cycle highs. Bitcoin then fell around 50% from its peak. The math on that sequence isn’t not complicated.

This is either a cyclical pressure test that the strongest holders survive, or it is the market disclosing that a leveraged, market-to-market-sensitive corporate Bitcoin treasury is structurally damaged by design. The rest of this article makes the case that it is closer to the latter.

MicroStrategy and Bitcoin Balance Sheet Mechanics Are Dangerous

Strategy, MicroStrategy’s rebranded entity, holds 843,706 BTC at an average acquisition value of about $75,599 per coin.

With Bitcoin declining toward $60,000 in the course of that period, that carries around $11 billion in unrealized losses. Every $1,000 move in BTC shifts Strategy’s paper position by $713.5 million.

Under updated FASB fair-value accounting rules in effect by 2026, those unrealized losses flow directly through net income, generating big negative EPS swings in quarterly filings.

For a company that has built its investor thesis wholly around Bitcoin accumulation, reporting multi-billion-dollar losses is not a rounding errors; it’s the product.

Across the eight largest pure-play Bitcoin treasury firms, controlling over 850,000 BTC integrated, unrealized losses had already exceeded $10 billion before the latest leg down.

Artemis data from February 2026 demonstrated system-level unrealized losses across corporate crypto portfolios surpassing $20 billion, even then, and no major corporate holder turned into in a net profit position on BTC at that point.

The market capitalization loss now visible across the sector isn’t a surprise outcome. It was a predictable one.

Investor Michael Burry has defined the dynamic as a “reflexive unwind”, falling BTC prices compress equity premiums, close the issuance window, and convert the model from collect-forever to sell-to-live on.

His situation analysis detects $60,000 as an existential crisis level for Strategy especially, where capital markets are correctly closed and multi-billion-dollar losses become locked instead of theoretical.